By Law Ka-chung

The Federal Reserve recently released a confusing signal to the market about their policy stance of being hawkish or dovish. This is expected given their “argument” that the bond market has done the tightening job for them.

Unless the Federal Reserve has lost credibility with the market, long-tenor Treasury yield should be a predictor of policy rate. That “argument” is tautological, where the Fed and the market mutually reference each other. The latest view given by Fed chair Jay Powell is that they are still not confident that inflation will really return to their 2 percent target.

They are worried about overdoing the hike given the long lag of policy effect as they always claim. True, monetary policy could take a long time to be effective ranging from two to three quarters to six plus quarters.

The rationale for such a long lag is that monetary tightening mainly cools investments, yet existing borrowings might not mature right after tightening but a few quarters afterward.

Only when the new funding costs are effective to the rollover of borrowings would the tightening impact be seen. Thus, how long needed depends on the outstanding borrowing tenors.

Another mechanism of inflation generation is not by way of borrowing or lending but by any economic transaction activities. While the former refers to investment, the latter refers to consumption.

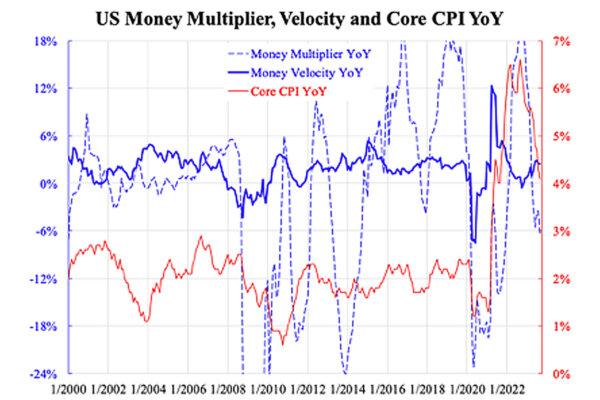

Since inflation is defined by consumer prices, the latter is supposed to be a more relevant factor. Yet the reality is case by case and depends on data. While borrowing or lending can be reflected by the money multiplier (broad-to-base money ratio), transactions can be seen from money velocity (nominal GDP to CPI ratio). Their growth rates can be compared with inflation.

The accompanying chart shows this. It suggests inflation (already excluding the volatile items of food and energy) is not very well explained by either of these two factors. This is because the two factors just capture monetary and goods aspects of aggregate prices with two simple theories behind them, yet there are many other markets and factors ignored in this analytical context.

More careful observation shows money multiplier is more relevant than money velocity in the recent round of inflation up and down. Money velocity is inversely related to core CPI (both in YoY growth) but is unlikely due to phase lag. While there could be a long time lag in investment (the so-called “time to build”), variables among the consumption market do commove. There could be supply-side factors in play, but if focused on the demand side, then the investment variables seem more relevant than the consumption ones. What, then, will be the implications?

As inflation is more investment-driven (money flow in investment than in consumption), a rate hike should be a better tool as investment is more interest-rate sensitive than consumption. It is indeed true that the time lag could be long. Yet whether tightening is enough can be judged from some investment activities like those in the housing market. Recent data seem to suggest some signs of investment rebound, which renders more potential tightening in the near future.